Having a good credit score benefits you in more ways than you may know. If your score isn’t where you want it to be, there are many incentives to making efforts to improve your credit score.

Having a good credit score benefits you in more ways than you may know. If your score isn’t where you want it to be, there are many incentives to making efforts to improve your credit score.

Unfortunately, having a bad credit score doesn’t just mean you’ll pay higher interest rates on your next loan. It can keep you from qualifying for a loan altogether, as banks and lenders will see you as being too high of a credit risk. Additionally, it can mean fewer opportunities for employment and renting as well as higher insurance and interest rates on your car loan and mortgage.

Especially in roles that involve handling money, it’s not uncommon for employers to run a credit check on you. If you don’t have a good credit score, you’re eliminating yourself from a lot of employment opportunities.

“If your credit score isn’t above 700, you simply just won’t get an interview [for these types of jobs],” states Charlie Scanlon, President of Phoenix Credit Consultants in St. Louis, Missouri. “Many don’t understand that it’s a gateway for them.”

The other place your credit score can impact you is in renting opportunities. Many high-end apartment complexes only consider applicants with credit scores above 700.

Your credit can also affect your liability insurance. Insurance companies utilize an insurance score, and a big part of your insurance score is the same factors that go into your credit score. Similarly, your homeowner’s liability insurance is going to be significantly more expensive if you have a poor score.

“Anybody can get an auto loan, but if you’ve got bad credit, you’re going to get an auto loan with an interest rate in the 20s,” Scanlon admits. “At this rate, statistically, you’re never going to pay that car off.”

In 2021, you must have a FICO credit score of at least 580 to qualify for an FHA loan with a 3.5% down payment. Conventional mortgage loans require a minimum score of 620. Even with the minimum score, you’re going to end up paying significantly more at a higher interest rate to qualify.

“The difference between a score in the 600s and 700s is, on a $200,000 house, you’re probably going to pay around $40,000 more for that house over the course of your mortgage,” Scanlon gives as an example.

It’s a really important tool, especially for young people, to understand what goes into a credit score. “For a young couple that learns what credit is and what it’s about, conservatively, it’s probably worth $100,000 to that couple throughout their lifetime, having a good credit score versus a bad one,” Scanlon estimates.

Luckily, it’s never too late for you to adopt good credit habits to help you continuously improve your credit score.

If you have no credit history, probably the only type of credit card you’ll be able to apply for is a secured credit card. These cards are specifically designed for people with little to no credit history to build their score.

The way that a secured card works is that a consumer makes a deposit into an account, and the bank or lending institution gives them a line of credit for that amount. If that person doesn’t use credit correctly or doesn’t pay their credit card back, the bank has a secured deposit against the line of credit that they’ve given them. They can easily pay back the bill and pay off the card if the person doesn’t follow through.

“The nice thing about secured credit cards is that they operate just like a normal credit card. The only difference is that the bank has no liability, whereas a traditional credit card is unsecured,” says Hillary Seiler, CFEd®, Certified Financial Coach and Credit Counselor, and Founder of Financial Footwork. “Secured credit cards operate the same way [as traditional cards] in that they build credit just as quickly as long as they’re used appropriately.”

One major benefit to a secured card is that there’s no credit check run when you apply. This not only guarantees your approval for the card but also ensures that your credit score won’t take a hit by an additional inquiry. “This eliminates the frustration of having to apply for different cards,” says Scanlon of Phoenix Credit Consultants. “Once you get your secured card, you want to use it properly and make your payments on time.”

Most cards require at least a $200 deposit, but some secured cards may even require a minimum deposit of $1000 or more. “You want to look for a card that doesn’t take a lot of your money from your deposit account,” Scanlon recommends. “It simply doesn’t make economic sense to tie [thousands of dollars] up interest-free in an account when you can do it for $200. Some secured cards will pay you nominal interest, but interest on that kind of an account is just hard to come by.”

If and when you decide that you no longer need to use the secured card, you get that deposit back. This allows you to use your money as a credit-building tool until you get your score high enough to apply for an ordinary credit card.

You’ll want to be sure that your secured credit card reports to all three national credit bureaus: Equifax, Experian, and TransUnion. Additionally, you’ll want to be sure that reporting occurs right away.

An authorized user is a person that is not legally obligated to pay on the card but has the account holder’s permission to use it. Authorized users get the benefit of the history and the utilization of that card, but the impact that it will have on their credit score will be less significant than it would be for the account holder.

“I recommend to people that they don’t go outside their immediate family or lifelong friends when opening authorized user accounts,” Scanlon warns. Account holders are liable for any charges made on the card, but if the account holder does not pay off their balance, it can have a negative impact on your score as an authorized user

Likewise, becoming an authorized user on an account held by someone with poor credit will not improve your credit score. Be sure that the account holder practices good credit habits and has a lengthy history of clean credit to maximize the benefit you’ll receive as an authorized user.

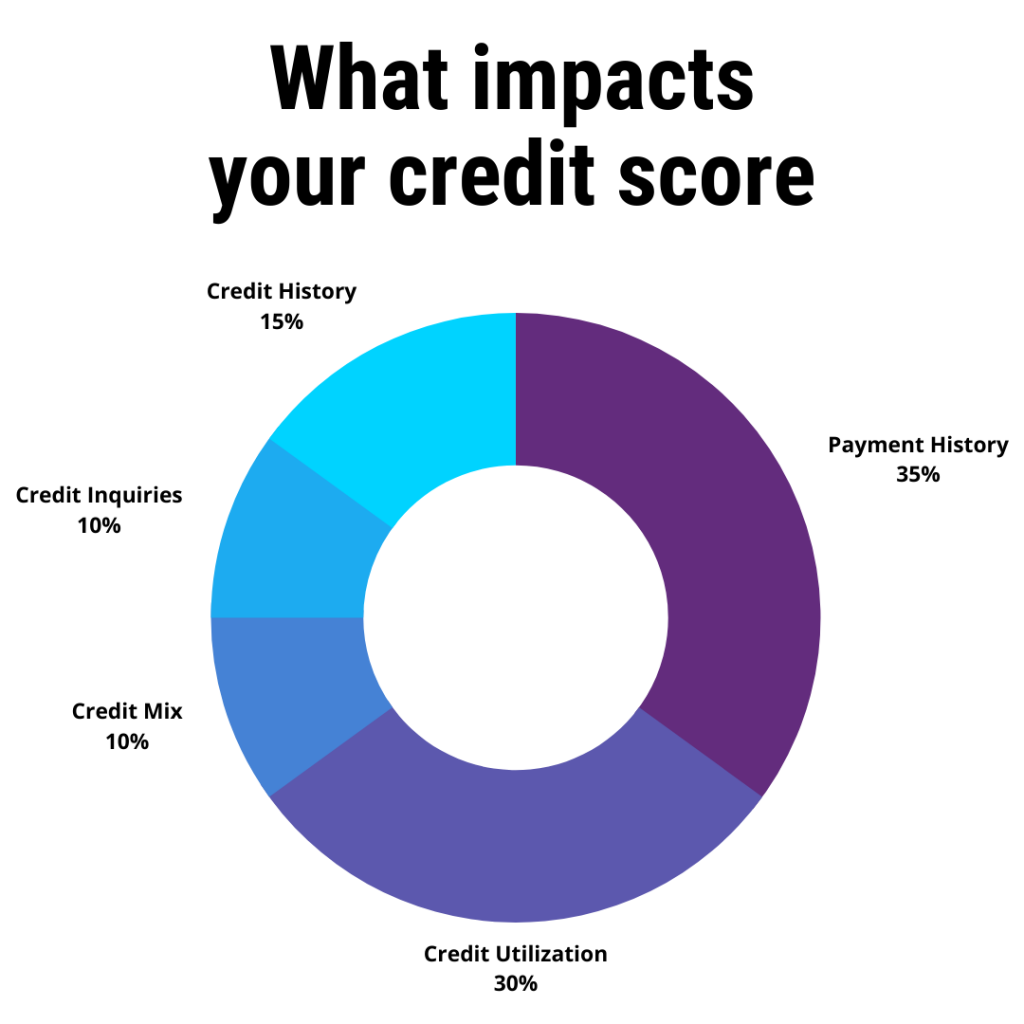

The credit algorithm is made up of five components: payment history is 35%, credit utilization is 30%, 10% is your mix of credit, and 10% is credit inquiries. The last 15% of your credit score is your credit history; if you close a credit card, you lose that history. “Your oldest credit card is your oldest friend — do not close your oldest credit card,” Seiler states.

If you are going to close a credit card, it should not be your oldest card, it should only be one that you’re not using. Still, be prepared for your score to dip a little. “Don’t open credit cards just to open them, and don’t close credit cards just to close them. Credit is a strategy game,” Seiler clarifies.

One exception to this rule might be if you’re in the rebuilding process and will be for years. In this case, you may want to just close the cards you aren’t using, including your oldest card, if you’re planning to restart from scratch

If you are in the building process, however, opening and closing cards will negatively impact you by not giving you the consistent history you need to improve your credit score. Plan and pick a card that you can use long-term and never close it.

Many credit cards offer rewards and promos to entice you to sign up. Cashback rewards, cash bonuses, and reduced APR perks are common and make it harder for you to say no. However, you should not be opening up a credit card simply to get the rewards. Rewards are best treated as a supplemental bonus to using your credit card responsibly.

“Don’t just open a credit card because they’re going to give you 20% off,” Seiler states. Credit cards are all about how you’re choosing to spend money and if you want to use credit on a regular basis to pay your bills.

For anyone that’s going to open a credit card, be strategic. Ask yourself, Why are you opening the card? Are you just opening it for the discount, or are you opening it because you will consistently use it every month?

You can check your credit score online for free each year. This is a great way to monitor your credit score and stay organized. Additionally, it can help protect you against fraud.

Despite common misconceptions, pulling your own credit report does not hurt your score. Companies like Credit Karma and Credit Sesame can be great resources for you to monitor your credit score without lowering it. On the other hand, having a lender pull your credit report does impact your score.

“My biggest tip is to set a reminder on your phone, and when that reminder comes, go to annualcreditreport.com, pull all reports for free, check and make sure they’re valid, and you’re good to go. It’s a great way to check your score and to make sure no one has stolen your identity,” Seiler explains.

Late credit card payments will not impact your credit score unless the payment is more than 30 days late. Once you reach a late payment of more than 30 days, it can take a big toll on your credit score.

The good thing is that the severity of that toll will lessen as time goes on. “Most of the time, if you only have one 30-day late, [prospective lenders] won’t be too worried about it,” Scanlon clarifies. However, if your payment is more than 60 days late, the damage will be more significant. Those types of late payments will continue to impact your score for seven years.

With the way the credit score algorithm is structured, there is a lessening of the penalty as time moves toward the end of that seven years, but you’ll continue to lose points for the time being. “Late pays are difficult to do anything with, even if it’s an honest mistake,” warns Scanlon. “Long term, the damage can be pretty significant.” Knowing this, you should employ thorough efforts to ensure your bills are paid on time.

Setting up your billing accounts on auto-pay and setting reminders on your phone are easy ways to stay on top of your payments and deadlines. Making micropayments — multiple payments over one billing cycle — can even be a great way to get in the habit of paying your bills on time, or even early.

You might believe that making micropayments helps to improve your credit score, but that’s not always the case. “Micropayments aren’t really going to do much for you unless you’re using more than 30% of your credit line,” adds Seiler. “This is why micropayments work well for some people and not others.”

Credit agencies don’t look at your credit weekly. Instead, they take a snapshot every two-to-four weeks; that’s when your credit score is generated. This explains why your score isn’t going to change when you’re paying off $20 weekly instead of just paying the payment in full once a month.

“Micropayments are fantastic when you’re just learning how to use credit,” Seiler says. However, they aren’t going to improve your credit score any more than just making your payments in full when your credit card statement goes out.

If you’re maxing your credit card out, you should in fact be making payments as quickly as you can. Seiler furthers, “That’s when micropayments can help to effectively improve your credit score because this lowers your payment utilization ratio.” Additionally, micropayments might benefit you more in terms of lowering your interest rate.

Practicing good habits will help you improve your credit score whether you’re starting from scratch or in the rebuilding process. “Credit is all about making your payments on time and using it consistently without maxing it out,” says Seiler. “So if you’re rebuilding credit, you need to be using it every single month, consistently.”

When dealing with a major misstep impacting your credit, such as bankruptcy, foreclosure, or if you have a long history of poor credit, Seiler’s first recommendation is to go get a secured credit and use less than 30% of the available limit each month.

“The biggest two factors are your credit history and your utilization, so if you’re not making your payments on time and you’re not using your credit correctly, you’re not going to have a good score,” she furthers. “This goes for anyone who’s building credit or coming back from a mishap, you need to make your payments on time, but you also need to maximize your credit utilization rule, which is: never use more than 30% of your line.

Basically, if you have $1000 on your line, you should never use more than $300 a month on your credit card because your score will drop after that 30% limit is used. “So even if you max out your credit card and you pay it back right away, your score will still drop. The credit bureau reads that as you not being responsible with your credit,” she explains.

While your credit doesn’t reflect who you are as a person, it does strongly represent how you come off to prospective banks, lenders, landlords, employers, and many others. Be sure to keep an eye on your credit score regularly to avoid the negative side effects of bad credit.

These tips can help you adopt good habits to improve your credit score, but if you have any questions regarding your credit concerns, reach out to a financial professional or credit counselor to learn more.

rebel Financial is a registered investment adviser and the opinions expressed by Phoenix Credit Consultants and Financial Footwork in this article are their own and do not reflect the opinions of rebel Financial. All statements and opinions expressed are based upon information considered reliable although it should not be relied upon as such. Any statements or opinions are subject to change without notice.

Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed.

Information expressed does not take into account your specific situation or objectives, and is not intended as recommendations appropriate for any individual. Readers are encouraged to seek advice from a qualified tax, legal, or investment adviser to determine whether any information presented may be suitable for their specific situation. Past performance is not indicative of future performance.

For more information, visit our disclosures page.

Get financial news, videos, free calculators, and other resources delivered straight to your inbox! Sign up for our newsletter to receive monthly updates from rebel Financial.

rebel Financial is a Registered Investment Advisor that provides retirement planning, estate planning, financial planning, and investment management services to individual and institutional clients. To get a more detailed description of the company, its management, and practices, view our (form ADV, Part2A) and Disclosures.

Fiduciary & Fee-Only Financial Advisors and Planners

All websites created by the rF marketing team