The disadvantages, if any, may stem from the financial trade-offs that a mortgage holder needs to make when paying off the mortgage. Paying it off typically requires a cash outlay equal to the amount of the principal. If the principal is sizeable, this payment could potentially jeopardize a middle-income family’s ability to save for retirement, invest for college, maintain an emergency fund, and take care of other financial needs.

If you have the financial means to pay off a mortgage, consider the following:

There is no “right” answer for everyone when it comes to potentially paying off a mortgage. Consider your feelings about debt, your timeline with respect to long-term goals, your tax savings, and other factors before making a decision that is in your best interest.

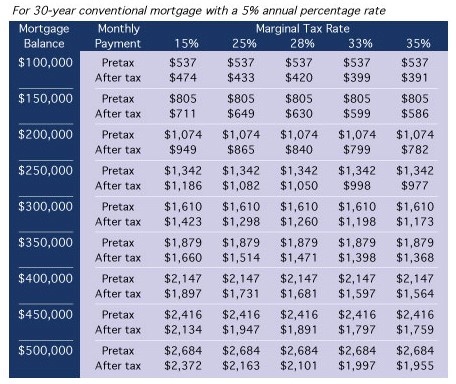

One of the big benefits of home ownership is the mortgage interest deduction. The federal government lets you deduct mortgage interest on a first or second home, up to $1 million per year.

Source/Disclaimer:

Source: Wealth Management Systems Inc. Monthly payments assume a conventional 30-year fixed-rate mortgage at 5% APR, excluding escrows for taxes, insurance, or other fees. Mortgage deductions are based on first month’s interest. Assumes that other deductions exceed the standard deduction. (CS0000218)

Because of the possibility of human or mechanical error by Wealth Management Systems Inc. or its sources, neither Wealth Management Systems Inc. nor its sources guarantees the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. In no event shall Wealth Management Systems Inc. be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of the content.

© 2015 Wealth Management Systems Inc. All rights reserved.