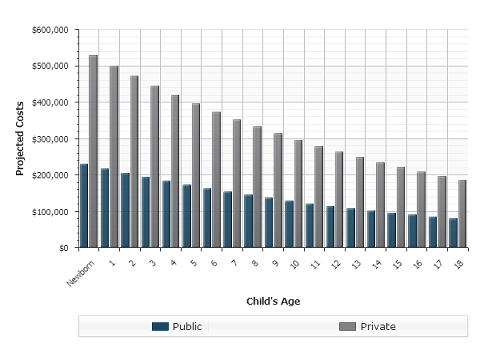

First the bad news: The cost of a college education has skyrocketed, increasing at a rates well above the general inflation rate in recent years. Now the good news: Your options for setting aside college money in tax-efficient investment accounts have increased as well. For example, in 2001 Congress enhanced 529 plans and Coverdell Education Savings Accounts (formerly known as Education IRAs). Other time-tested strategies, such as contributing to a minors custodial account (UGMA/UTMA accounts), continue to offer potential benefits as well.

The Lowdown on 529 Plans

Created in 1996 and named after the section of the federal tax code that governs them, 529 plans are generally sponsored by individual states, but in some cases may also be sponsored by qualified educational institutions. They are administered by investment companies, which also oversee the underlying investments. There are two types of 529 plans:

Prepaid tuition plans let participants pay for future tuition at today’s rates, essentially taking inflation out of the equation. These plans are generally available only to residents of the sponsoring state and may be intended for in-state tuition (participants may be able to use the money at out-of-state schools, but only a reduced percentage of the balance in some cases).

College savings plans — the focus of this article — let participants invest their contributions in portfolios of mutual funds or similar managed financial instruments. Money in a college savings plan can be used for qualified undergraduate and graduate expenses at any accredited college or university. Many of these plans are national plans: No matter which state or school sponsors them, residents of any state can participate. With some 529 college savings plans, contributions are allocated to a particular portfolio based on the child’s age. As the child nears college age, the money shifts to different portfolios with appropriate risk and return potential. Other 529 plans offer greater investment flexibility, letting the account holder choose from a range of securities.

The potential advantages of 529 plans include:

Tax-free earnings — Earnings in a 529 plan accumulate free from taxes, and qualified withdrawals are federally tax free. Withdrawals may be exempt from state taxes as well (tax rules vary from state to state). Nonqualified withdrawals from a 529 plan may be subject to income taxes and a 10% additional federal tax.

Gift tax benefits for contributors — A contribution to a 529 plan is considered a gift for federal tax purposes. Tax rules currently let you give up to $14,000 in 2015 to as many individuals as you choose, free from federal gift taxes. Gifting schedules can also be accelerated through a lump-sum contribution of $70,000 to a 529 plan in the first year of a five-year period.

Generous contribution rules — Lifetime contribution limits on 529 plans vary from state to state, but often exceed $200,000 per beneficiary, including earnings. In addition, there usually are no income restrictions on contributors to a 529 plan.

Account control — The individual who creates a 529 plan account on behalf of a beneficiary generally maintains complete control over the account. This is not the case with Coverdell Education Savings Accounts or certain types of custodial accounts. Account owners may also change beneficiaries.

Finally, contributions to 529 plans may provide a state tax deduction for residents of the sponsoring state.

To identify the 529 plan that best suits your needs, ask the following questions about each one you evaluate: Can you transfer account ownership? What are the contribution limits? Are the investment choices appropriate for your needs? Are there any fees? Is your intended school considered a qualified institution by the IRS? You may also want to work with a financial advisor to narrow down your options.

UGMA/UTMA Accounts: Awarding Custody

Of course, not all college savings strategies require the involvement of a college or a state government. For example, by following the guidelines established under the Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) — each state uses one or the other — adults such as parents and grandparents can establish and contribute to a custodial account in a minor’s name without having to establish a trust or name a legal guardian.

Contributing to an UGMA/UTMA account can accomplish two goals simultaneously: helping a future student prepare for college costs and reducing the value of a contributor’s taxable estate. UGMA/UTMA accounts also offer favorable tax treatment of investment earnings. For example, the first $1,000 of earnings is tax free each year. If the minor is under 19, earnings in excess of $1,000 but not above $2,000 are taxed at the child’s rate. If earnings exceed $2,000 for children under 19, the income is taxed at either the parents’ rate or the child’s rate, whichever is higher. If the child is older than 19, all income is taxed at his or her rate. Note that the age limit increases to 24 for a full-time student if the child doesn’t have earned income in excess of half of his or her annual support.

Despite the obvious appeal of UGMA/UTMA accounts, it’s worth noting that the assets in the account belong to the child, not to the contributor. When the child reaches legal adulthood at age 18 or 21, depending on the state, he or she is free to spend the money with no restrictions. In other words, contributors cannot force that individual to use the money for college costs.

Coverdell: New Name, Better Benefits

The Education IRA, as we knew it, had a relatively short life. In 2002, just five years after its creation, the popular college savings account was renamed the Coverdell Education Savings Account, after the late Senator Paul Coverdell. But that’s not the only change worth noting. Contribution limits also increased, income eligibility for married taxpayers rose, and the range of eligible education expenses expanded considerably.

Coverdells are qualified investment accounts that allow nondeductible contributions of up to $2,000 annually per beneficiary. Earnings in the account are not taxed, and as long as withdrawals are used for qualified education expenses, they are tax free as well. Assets in a Coverdell must be used before the beneficiary’s 30th birthday. Keep in mind that the designated beneficiary of a Coverdell account is free to take withdrawals at any time, but any amount in excess of his or her qualified education expenses will be taxable as income. A 10% additional federal tax may also apply.

Coverdells also have a special feature unavailable with 529 plans: Qualified withdrawals may be used to pay for an elementary, secondary, or college education. Withdrawals from 529 plans can only be used for college expenses. Unlike 529 plans, Coverdells impose income eligibility limits on contributors. Single filers with modified adjusted gross incomes of more than $110,000 and joint filers with incomes of more than $220,000 cannot contribute.

The deadline to contribute to a Coverdell is generally April 15, the same deadline that applies to IRAs. Before making a decision about a Coverdell, evaluate the investment options, fees, and services offered by competing financial institutions that provide the accounts.

Finally, when choosing a college investment vehicle, remember that it may not be a “one or the other” decision. It may make sense for you to contribute to more than one type of account simultaneously. Speak with a financial and tax advisor about your particular needs.

529 college savings plans let participants invest money in portfolios of mutual funds or similar investment vehicles to be used for qualified undergraduate and graduate expenses at any accredited college or university. They offer the potential for tax-free withdrawals and a wide range of other features and benefits.

UGMA/UTMA custodial accounts may offer estate tax breaks to contributors, as well as income tax breaks. However, when the minor reaches the legal age of adulthood, the money can be spent however he or she chooses.

Coverdell Education Savings Accounts allow tax-free growth and withdrawals of earnings for qualified expenses, but contribution and income limits may restrict their effectiveness for some taxpayers.

Unlike 529 plans, Coverdells allow tax- and penalty-free withdrawals for elementary and high school expenses, in addition to college expenses.

This article was written for information purposes only and its content should not be construed by any consumer and/or prospective client as rebel Financial’s solicitation to affect, or attempt to affect transactions in securities, or the rendering of personalized investment advice for compensation. No client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from rebel Financial, or from any other investment professional. See our disclosures page for more information.

Phil Ratcliff, President of rebel Financial, is a senior financial advisor that holds an AIF®, CFP®, ChFC®, and CLU® certifications. He started his career at American Express Financial Advisors in 2003, then moved to AXA Advisors for 7 years before founding rebel Financial LLC in 2013.