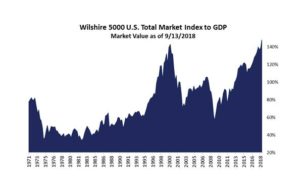

What else has changed? In the past, stock traders watched the ratio of the total value of the U.S. stock market to the total U.S. GDP, as an indicator of when the market was becoming dangerously overvalued. You can see this ratio over the years in the accompanying chart, going back to 1971, and indeed in the runup to the great tech crash, this indicator was sending sell signals. It was also sending lesser signals during the runup to the 2008-2009 market decline. And today—oh boy…

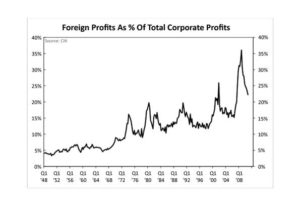

What else has changed? In the past, stock traders watched the ratio of the total value of the U.S. stock market to the total U.S. GDP, as an indicator of when the market was becoming dangerously overvalued. You can see this ratio over the years in the accompanying chart, going back to 1971, and indeed in the runup to the great tech crash, this indicator was sending sell signals. It was also sending lesser signals during the runup to the 2008-2009 market decline. And today—oh boy… How could things be different today than in the past? The next chart shows that, over time, American companies have been generating a growing amount of their profits overseas, which means that comparing their value to the strictly U.S. economy—where only somewhere between 65% and 80% of their profits are coming from—becomes less relevant. The signal may have meant something the past, but today it is increasingly meaningless.

How could things be different today than in the past? The next chart shows that, over time, American companies have been generating a growing amount of their profits overseas, which means that comparing their value to the strictly U.S. economy—where only somewhere between 65% and 80% of their profits are coming from—becomes less relevant. The signal may have meant something the past, but today it is increasingly meaningless.

rebel Financial is a Registered Investment Advisor that provides retirement planning, estate planning, financial planning, and investment management services to individual and institutional clients. To get a more detailed description of the company, its management, and practices, view our (form ADV, Part2A) and Disclosures.

Fiduciary & Fee-Only Financial Advisors and Planners