Focus on Time in the Market, Not Market Timing. Sports commentators often predict the big winners at the start of a season, only to see their forecasts fade away as their chosen teams lose. Similarly, market timers often try to predict big wins in the investment markets, only to be disappointed by the reality of unexpected turns in performance. It’s true that market timing sometimes can be beneficial for seasoned investing experts (or for those with a lucky rabbit’s foot); however, for those who do not wish to subject their money to such a potentially risky strategy, time — not timing — could be the best alternative.

What Is Market Timing?

Market timing is an investing strategy in which the investor tries to identify the best times to be in the market and when to get out. Relying heavily on forecasts and market analysis, market timing is often utilized by brokers, financial analysts, and mutual fund portfolio managers to attempt to reap the greatest rewards for their clients.

Proponents of market timing say that successfully forecasting the ebbs and flows of the market can result in higher returns than other strategies. Their specific tactics for pursuing success can range from what some have termed “pure timers” to “dynamic asset allocators.”

Pure timing requires the investor to determine when to move 100% in or 100% out of one of the three asset classes — stocks, bonds, and money markets. Investment in a money market fund is neither insured nor guaranteed by the U.S. government, and there can be no guarantee that the fund will maintain a stable $1 share price. The fund’s yield will vary. Perhaps the riskiest of market timing strategies, pure timing also calls for nearly 100% accurate forecasting, something nobody can claim.

On the other hand, dynamic asset allocators shift their portfolio’s weights (or redistribute their assets among the various classes) based on expected market movements and the probability of return vs. risk on each asset class. Professional mutual fund managers who manage asset allocation funds often use this strategy in attempting to meet their funds’ objectives.

Market Timing Has Its Risks

Although professionals may be able to use market timing to reap rewards, one of the biggest risks of this strategy is potentially missing the market’s best-performing cycles. This means that an investor, believing the market would go down, removes his investment dollars and places them in more conservative investments. While the money is out of stocks, the market instead enjoys its best-performing month(s). The investor has, therefore, incorrectly timed the market and missed those top months. Perhaps the best move for most individual investors — especially those striving toward long-term goals — might be to purchase shares and hold on to them throughout market cycles. This is commonly known as a “buy and hold” investment strategy.

As seen in the accompanying table, purchasing investments and then withstanding the market’s ups and downs can work to your advantage. Though past performance cannot guarantee future results, missing the top 20 months in the 30-year period ended December 31, 2014, would have cost you $20,546 in potential earnings on a $1,000 investment in Standard & Poor’s Composite Index of 500 Stocks (S&P 500). Similarly, a $1,000 investment made at the beginning of 1995 and left untouched through 2014 would have grown to $6,548; missing only the top 20 months in that span would have cut your accumulated wealth to $1,436.1

Though many debate the success of market timing vs. a buy-and-hold strategy, forecasting the market undoubtedly requires the kind of expertise that portfolio managers use on a daily basis. Individual investors might best leave market timing to the experts — and focus instead on their personal financial goals.

The Risk of Missing Out |

| | 1985-2014 | 1995-2014 | 2005-2014 |

| [1] | Untouched | $25,109 | $6,548 | $2,094 |

| [2] | Miss 10 Top-Performing Months | 9,650 | 2,796 | 998 |

| [3] | Miss 20 Top-Performing Months | 4,563 | 1,436 | 639 |

Perhaps the most significant risk of market timing is missing out on the market’s best-performing cycles. The three columns represent the growth of a $1,000 investment beginning in 1985, 1995, and 2005, and ending December 31, 2014. Row 1 shows the investment if left untouched for the entire period shown above; Row 2 shows the investment if it was pulled out during the 10 top-performing months; and Row 3 shows the investment if it was pulled out during the 20 top-performing months. |

Use Time to Your Advantage

If you’re not a professional money manager, your best bet is probably to buy and hold. Through a buy-and-hold strategy, you take advantage of the power of compounding, or the ability of your invested money to make money. Compounding can also help lower risk over time: As your investment grows, the chance of losing the original principal declines.

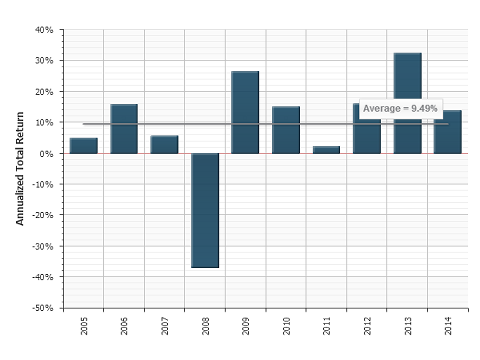

Annual Return of the S&P 500 |

|

| Source: ChartSource®, Wealth Management Systems Inc. For the period from January 1, 2005, through December 31, 2014. Average is calculated using full calendar years only. Past performance is not a guarantee of future results. It is not possible to invest directly in an index. Copyright © 2015, Wealth Management Systems Inc. All rights reserved. Not responsible for any errors or omissions. (CS000141) |

Regular Evaluations Are Necessary

Buy and hold, however, doesn’t mean ignoring your investments. Remember to give your portfolio regular checkups, as your investment needs will change over time. Most experts say annual reviews are enough to ensure that the investments you select will keep you on track to meeting your goals.

Normally a young investor will probably begin investing for longer-term goals such as marriage, buying a house, and even retirement. The majority of his portfolio will likely be in stocks and stock funds, as history shows they have offered the best potential for growth over time, even though they have also experienced the widest short-term fluctuations. As the investor ages and gets closer to each goal, he or she will want to re-balance portfolio assets as financial needs warrant.

This hypothetical investor knows that how much time is available plays an important role when determining asset choice. Most experts agree that a portfolio made up primarily of the “riskier” stock funds (e.g., growth, small-cap) may be best for those saving for goals more than five years away; growth and income funds and bond funds might be the main focus for investors nearing retirement or saving for shorter-term goals; and investors who see a possible need for cash in the near future might consider a portfolio weighted toward money market instruments.2 Remember, though, that even those enjoying retirement should consider the historical inflation-beating benefits of stocks and stock mutual funds, as people often live 20 years or more beyond their last official paycheck.

Time Is Your Ally

Clearly, time can be a better ally than timing. The best approach to your portfolio is to arm yourself with all the necessary information, and then take your questions to a financial advisor to help with the final decision making. Above all, remember that both your long- and short-term investment decisions should be based on your financial needs and your ability to accept the risks that go along with each investment. Your financial advisor can help you determine which investments are right for you.

Source/Disclaimer:

1Source: Wealth Management Systems Inc. Stocks are represented by Standard & Poor’s Composite Index of 500 Stocks, an unmanaged index generally considered representative of the U.S. stock market. Individuals cannot invest in indexes. Past performance is not a guarantee of future results.

2An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although most funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund.

Because of the possibility of human or mechanical error by Wealth Management Systems Inc. or its sources, neither Wealth Management Systems Inc. nor its sources guarantees the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. In no event shall Wealth Management Systems Inc. be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of the content.

© 2015 Wealth Management Systems Inc. All rights reserved.